The lending industry stands at crossroads. Traditional underwriting methods built on manual reviews and rigid scorecards no longer deliver the ability of lenders’ needs. With rising competition and increasing regulatory scrutiny, relying on outdated tools can lead to missed opportunities and higher risks.

In this environment, risk-based lending becomes a fulcrum of advantages. It means making decisions that are personalized, context-aware, and dynamically aligned with borrower risk. The game-changer? Technology and data intelligence. With modern loan management software, lenders are not just automating processes; they are embedding intelligence into underwriting, servicing, and portfolio management.

When you think in these terms, the notion of “risk-based lending” moves from being an operational exercise to strategic capability. And the right loan servicing software becomes more than a tool: it becomes a differentiator.

In this blog, we explore how risk-based lending works, where traditional methods fall short, and how modern software supports it. We also provide practical use cases of data intelligence, including tangible business outcomes and guidance on getting started.

Table of Content

- What Is Risk-Based Lending?

- What Are the Challenges in Traditional Risk-Based Lending?

- How Does Loan Management Software Enable Risk-Based Lending?

- How Does Data Intelligence Create Real-World Impact?

- What Tangible Business Outcomes Do Lenders Enjoy Upon Adopting Loan Management Software?

- How Can Lenders Begin Their Risk-Based Lending Journey?

- Why Should Lenders Consider LoansNeo?

- Conclusion

What Is Risk-Based Lending?

At its essence, risk-based lending involves pricing loans and determining eligibility based on the borrower’s risk profile, rather than applying a one-size-fits-all interest rate or underwriting rule. You ask: What factors determine that profile?

Typical factors include:

- Credit history (past repayment behavior, delinquencies)

- Income stability (job tenure, business cash flows)

- Repayment patterns (EMIs, overdue, prepayments)

- Market conditions (economic cycles, sector stress)

- Other contextual signals (alternate data, behavioral data)

Historically, lenders used rule-based underwriting: for example, “if credit score > X and DTI < Y then approve”. That approach works to some extent, but is static, coarse-grained, and brittle in changing environments.

Now, with data-driven predictive models, lenders can shift from “yes/no” decisions based on fixed rules to nuanced decisions based on probabilistic risk, real-time signals, and borrower segmentation. In other words, risk-based lending has matured into dynamic risk-sensitive decision-making.

Interestingly, the global credit risk assessment market is growing rapidly, expected to rise from USD 9.55 billion in 2025 to USD 31.46 billion by 2034, at a CAGR of 14.17%. This growth shows how technology-driven risk models are becoming central to modern lending.

What Are the Challenges in Traditional Risk-Based Lending?

Why isn’t risk-based lending doing everything it could already? This is because traditional approaches have several limitations. The common challenges in traditional risk-based lending include:

- Fragmented Borrower Data Sources: Many lenders still rely on credit bureau scores, income statements, and application forms as primary sources of borrower data. But the borrower’s financial ecosystem is larger and more complex. Without the full view, risk is misestimated.

- Manual Scoring Models and Spreadsheets: Underwriting teams often maintain scorecards, spreadsheets, and manual reviews. That means many decisions are slow, inconsistent, and unfriendly to audits.

- Limited Visibility Across the Loan Lifecycle: A loan, once disbursed, is often out of view, except for simple delinquency tracking. Early signs of stress (behavioral changes, external signals) are missed.

- Difficulty Identifying Early Signs of Default Risk: Without behavioral monitoring or continuous data feeds, the risk of default becomes visible only when it is too late to act.

- Slower Decision-Making Means Lost Customers: In a world where borrowers expect speed and flexibility, a slow “approve or reject” system based on old data means missed opportunities.

A recent study shows that 70% of financial institutions have automated consumer lending, but only one-third have achieved similar automation for SMB lending. This gap creates significant inefficiencies for a substantial portion of the lending market. These challenges set the stage for a solution: modern loan management software that integrates data intelligence and supports risk-based lending in real time.

Did You Know? The first recorded loan in history dates back over 4,000 years to ancient Mesopotamia, where farmers borrowed seeds and repaid with crops.

How Does Loan Management Software Enable Risk-Based Lending?

“Over the last decade and a half, the notion of digital tools, decisioning, analytics and underwriting has come into play. The COVID-19 pandemic has dramatically accelerated that, and we’re seeing three big trends shake up the financial services industry,” Shri Santhanam, Executive Vice President and General Manager of Global Analytics and Artificial Intelligence (AI), Experian.

A robust loan processing software creates an intelligent ecosystem that connects data, decisions, and compliance, fostering a seamless workflow. It’s essential to consider the capabilities, not just the features, of robust loan management software. Here’s how these systems deliver strategic value.

| Capability | KeyValue Delivered Milestones |

|---|---|

|

Unified Borrower Data Layer |

Integrates all borrower data, such as credit history, statements, and alt data into one risk view, eliminating silos |

|

Automated Credit Scoring Models |

Applies consistent, auditable scoring without manual spreadsheets, reducing decision bias and human error |

|

Risk-Based Pricing Rules |

Enables dynamic interest rates and loan terms aligned with borrower risk levels. Safer borrowers benefit, while riskier profiles get priced appropriately. |

|

Continuous Loan Tracking and Behavioral Analytics |

Monitors repayment behavior, transaction trends, and deviations to detect early risk or fraud |

|

Portfolio-Level Risk Dashboards |

Gives CXOs portfolio visibility into heat maps, risk concentration, and what-if scenarios to manage exposure and capital proactively |

To sum it up, modern loan servicing software turns risk-based lending from a static policy into a dynamic, data-driven discipline. Speed, accuracy, compliance, and scalability all improve.

How Does Data Intelligence Create Real-World Impact?

Data intelligence changes the game from reaction to prediction. To see data intelligence in action, it is essential to explore a few real-world scenarios where modern loan tracking software makes lending smarter. Here are the popular real-world use cases:

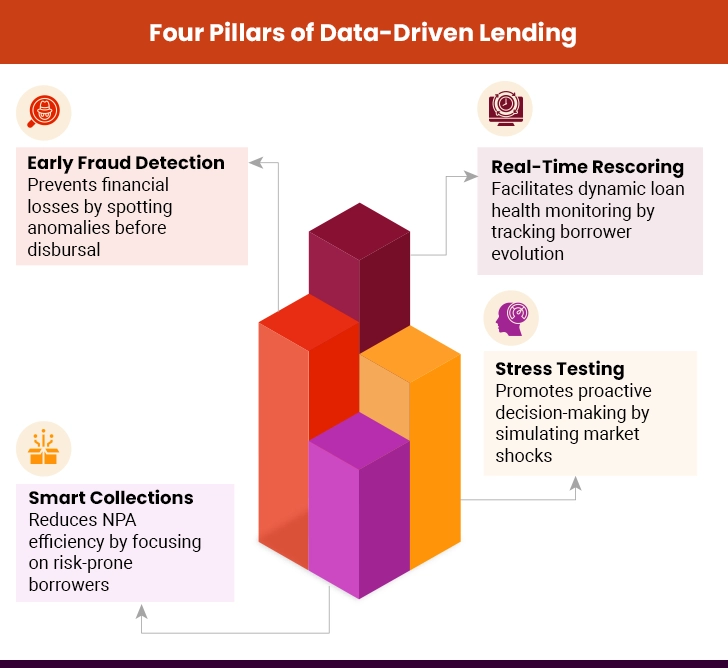

Use Case 1: Early Fraud Detection via Pattern Analysis

Imagine a borrower submits plausible documents, but the system flags unusual patterns: identical bank statement data across multiple applications, sudden income spikes, anomalous transaction patterns. The loan management software, which integrates alternative data and applies to machine learning, flags this as a potential risk of fraud. The lender can hold the application, verify further, or decline, thereby reducing losses before disbursement.

Use Case 2: Real-Time Rescoring During Loan Lifecycle

A borrower’s risk profile doesn’t stay static. Suppose six months into the loan, their bank account transaction flow drops significantly, or new negative bureau entries appear. The system automatically re-scores the borrower and triggers a medium-risk flag. The lender may then alter conditions, contact the borrower for advice, or adjust collections. This responsiveness is possible only when commercial loan origination software links behavior data, underwriting data, and alerts.

Use Case 3: Automated Collections Prioritization (Which Customer to Call First)

In an extensive portfolio, you cannot call everyone at once. The system utilizes behavioral analytics to identify which customers are most likely to default in the near term, based on changes in repayment behavior, external signals, sector stress, and other factors. Collections teams receive a ranked list, and they contact the high-risk borrowers first, thereby improving efficiency and reducing non-performing assets (NPAs).

Use Case 4: Portfolio Stress Testing During Economic Shifts

A lender wants to model the impact of a 2% interest rate rise and a 3% increase in unemployment in a key sector. The loan management software enables the risk team to run stress scenarios across the portfolio, simulating the impact on various borrower segments. They can spot weak clusters, decide to reduce new exposure, or set aside higher provisions. This transforms risk-based lending into strategic thinking, rather than just transactional underwriting.

To better understand how lenders can make smarter, faster, and safer credit decisions, here are the four key pillars that define data-driven lending in action.

What Tangible Business Outcomes Do Lenders Enjoy Upon Adopting Loan Management Software?

When you adopt risk-based lending underpinned by data intelligence and robust loan servicing software, the benefits are both strategic and operational. They range from improved productivity to reduced risks. Let’s enumerate key outcomes and explain them.

I. Reduced NPAs and Delinquencies

By identifying risk earlier, monitoring borrower behavior, and intervening sooner, you reduce defaults. The sooner you see the problem, the lower the loss. A unified data-driven view means fewer surprises.

II. Faster Time-to-Yes for Qualified Borrowers

Borrowers who are at low risk no longer wait for lengthy approvals. Automated scoring and integrated data reduce cycle time. Speed is a competitive edge. When you say yes quickly to the right borrowers, you win business.

III. Lower Operational Risk and Underwriter Dependency

With automated models, alerts, dashboards, and workflows, you reduce manual decision-making, spreadsheet errors, and dependence on individual underwriters. The process becomes scalable and auditable.

IV. Higher Profitability via Risk-Adjusted Pricing

When you price loans based on risk, you align interest income with expected risk. Riskier borrowers pay more, whereas safer ones pay less. This smart risk-adjusted pricing improves profit margins.

V. Better Audit, Compliance, and Board Reporting

Modern software for loan servicing provides comprehensive workflows, decision trails, and dashboards. Compliance is baked in, and executives get clear visibility. That strengthens credit discipline and regulatory posture. A strategic lender uses this as a competitive advantage, not just a cost.

In short, data-driven risk management becomes a competitive advantage. Not just because you reduce losses, but because you make smarter credit decisions, faster, more reliably, and scale them. The following table captures why businesses are moving to intelligent lending.

Manual vs Intelligent Lending

| Aspect | Traditional Approach | Data-Driven Approach DeliveredMilestones |

|---|---|---|

|

Decision Speed |

Manual, slow |

Instant, analytics-driven |

|

Risk Assessment |

Static rule-based |

Continuous and adaptive |

|

Pricing |

Flat interest rate |

Dynamic risk-based pricing |

|

Compliance |

Manual tracking |

Automated reporting |

How Can Lenders Begin Their Risk-Based Lending Journey?

Adopting this approach doesn’t mean tearing down everything at once. One must start practically and scale gradually. If you are a lending institution (bank, NBFC, fintech) and you want to adopt this path, here is a pragmatic roadmap.

1. Ensure Data Quality and Governance Framework

You cannot build intelligence on junk data. Define governance: data ownership, data cleansing, data standardization, and alternative data sources. Ensure that the correct data is fed into your loan servicing software. Start with a data audit: what sources do you have, what gaps exist?

2. Start with Hybrid Models: Rule-Based + Predictive

You don’t need to throw away everything and start from scratch. Many lenders begin by using their existing rules, which are embedded in their systems, and then overlay predictive risk models. Over time, you calibrate and move to more advanced analytics. This hybrid approach allows for a gradual transition.

3. Integrate LMS with External Credit Data Sources

Ensure your loan management system integrates with credit bureaus, bank statements, GST/tax data, and alternative data sources (telemetry, cash flow, behavior). Integration is crucial.

4. Roll Out Risk Scorecards Gradually by Segment

Pick a manageable segment (say, small business loans up to a specific size) and implement your new risk-based lending process there. Monitor performance, refine models, and capture insights. Thereafter, you can scale to other segments. This avoids wholesale disruption and lets you demonstrate early wins.

5. Build a Continuous Monitoring and Feedback Loop

Once loans are disbursed, ensure the system tracks borrower behavior, external signals, and flags any changes in risk. Create feedback loops: what are the defaults? How accurate was the model? Use that to refine scoring and decision logic.

6. Change Management and Culture

Technology is only part of the equation. Your underwriting and collections teams must trust and adopt the system. Provide training and communicate the “why” (data-driven risk is a competitive advantage). Encourage teams to use dashboards, act on alerts, and engage proactively with borrowers.

7. Choose the Right Loan Management Software

There is a range of solutions available on the market, each catering to different needs. As such, it is essential to select the right loan management software. When evaluating software for loan servicing, loan management, loan origination, or loan processing, ask for:

- Real-time analytics and dashboards

- Configurable scoring/rule engines

- Integration capabilities (APIs) with external data

- Behavioral monitoring and early warning modules

- Scalability (cloud-based, modular architecture) allows your risk-based lending model to grow

Did You Know? The first recorded loan in history dates back over 4,000 years to ancient Mesopotamia, where farmers borrowed seeds and repaid with crops.

Why Should Lenders Consider LoansNeo?

Moving from spreadsheets and manual checks to innovative, data-driven lending takes the right system. LoansNeo is one such platform that helps lenders manage the entire loan lifecycle, from application to repayment, with clarity, speed, and control.

- Unified Borrower View: It brings together all borrower data, from origination to servicing, in one place. This helps lenders see the complete risk picture and make confident decisions.

- Automated Workflows: Loan software replaces manual steps with digital ones. Applications move smoothly through approvals, document checks, and disbursement, reducing errors and delays.

- Built-In Analytics and Dashboards:The platform tracks repayment behavior, portfolio trends, and risk patterns in real time. Lenders can identify early warning signs and take action before risk turns into a loss.

- Flexible and Connected: LoansNeo seamlessly integrates with other tools, including credit bureaus, accounting software, and payment systems. This keeps data flowing without friction.

Conclusion

Risk-based lending powered by data intelligence and modern loan servicing software is no longer optional. It’s a strategic imperative for lenders who want to stay ahead. Traditional underwriting, spreadsheets, and manual models are simply unable to keep pace with the evolving needs of the industry.

By embracing a unified data view, automated modelling, dynamic pricing, continuous monitoring, and portfolio-level risk insights, lenders can improve borrower evaluation accuracy, reduce NPAs and defaults, scale responsible lending, and strengthen compliance and credit discipline. In short, data-driven risk is a competitive advantage.

If you are in the business of lending, now is the time to ask: Are we just using software to process loans faster, or are we using software to lend smarter?