Imagine a policyholder’s car breaks down on a rainy evening. Instead of calling a helpline and waiting endlessly, their insurer automatically detects the incident, dispatches roadside assistance, and initiates the claim, all before the customer even asks. Sounds like science fiction? Not anymore.

The insurance industry is changing fast. What used to be largely reactive, paper-filled, and slow is now morphing into something far more dynamic. The old way of underwriting, processing claims, and servicing policyholders is under intense pressure. Customer expectations have shifted; risks have grown more complex, and regulations keep tightening. At the same time, the data landscape has exploded: insurers now have vast volumes of customer behavior, asset data, risk indices, and IoT inputs. But having data is not the same as acting on it.

That’s where the advent of AI in Salesforce and allied digital platforms becomes a pivotal turning point. Insurers who were once challenged by legacy silos now have the chance to reinvent themselves. They can move from product-centric to customer-centric, from reactive claims to predictive prevention, from manual to automated, and from fragmented to integrated.

In this blog, we explore the pain points of insurance, how the Salesforce ecosystem, specifically its intelligence-led capabilities, fits in, real-world use cases, the adoption of roadmap, and the future that awaits.

What Are the Major Pain Points in the Insurance Industry?

Even as investment in technology has grown, many insurers still struggle with structural issues. These issues largely stem from stringent regulations, rising customer expectations, and rapid technological innovation. Let’s break down some of the major pain points.

1. Fragmented Customer Data

Many insurers have built their systems over the years. Customer data lives in disparate places: legacy CRMs, spreadsheets, policy admin systems, third-party portals, and even sticky notes. The same customer might appear under multiple reference IDs or across business units, making a holistic view difficult to achieve. Without a single “golden record” of the customer, true personalization is hard. Upshot: slow service, erroneous renewals, policy overlaps or gaps, and sub-optimal cross-sell or retention offers.

2. Inefficient Claims and Underwriting

Underwriting and claims remain labor-intensive. They’re riddled with manual review of documents, human validation of risk factors, error-prone entry of data, and long turnaround times for decisions. Claims get stuck in bottlenecks; adjusters spend time chasing missing information, and customers face delays or poor communication. These inefficiencies cost in terms of operational expenses, customer dissatisfaction, and sometimes compliance exposure.

3. Customer Experience Gaps

Customers expect slick digital experiences. They expect insurers to know them, anticipate their needs, converse in context, and act quickly. This is where many insurers lag, as one in two policyholders finds the customer experience underwhelming. Lack of personalization results in generic outreach, while delayed communication makes customers feel ignored or undervalued. When a claim is filed, customers want real-time status updates, not vague promises. When a renewal is due, they want relevant offers, not generic mailshots.

4. Regulatory Pressures and Risk Management

Insurers operate in a highly regulated environment. This compliance comes with solvency rules, risk modeling standards, customer disclosure rules, and data privacy laws. At the same time, innovation is being pushed. This includes new products, usage-based insurance, embedded insurance, and parametric models.

Balancing innovation with risk governance is tricky. Over-automation might expose blind spots; under-automation might lead to inefficiency and increased costs. Risk management itself now involves new exposures (cyber, climate, IoT) that require richer data and faster insight.

Did You Know? The earliest known insurance contract dates to Genoa in 1347. Over the following century, maritime insurance grew rapidly, with premiums adjusted intuitively based on the level of risk.

5. Data Without Intelligence

Many insurance teams collect mountains of data: customer profiles, claims histories, external risk indices, IoT sensor feeds, and telematics. But data alone isn’t enough. Without the ability to derive insight, automate decisions, predict outcomes, or personalize offers, the data sits idle. Analytics may be ad-hoc or limited to reporting, not embedded into operational workflows. Hence, the promise of “data-driven insurance” sometimes remains unfulfilled.

Let’s have a look at the impact of these common pain points.

Pain Points vs. Business Impact

| Pain Point | Common Cause | Impact |

|---|---|---|

|

Fragmented Data |

Disparate, legacy systems |

Delayed insights |

|

Manual Underwriting |

Paper-based workflows |

Longer turnaround times |

|

Compliance Pressure |

Frequent rule changes |

Risk of non-compliance |

|

Data Without Intelligence |

Siloed analytics |

Missed opportunities |

Together, these pain points provide the urgent impetus for transformation, not just incremental digital projects, but a rethink of how insurance operates in a world where speed, relevance, and automation matter.

What Is Salesforce AI and What Does It Bring to Insurance?

Salesforce AI refers to a suite of artificial intelligence technologies, including generative AI, machine learning (ML), and natural language processing (NLP). It helps organizations with predictive analytics, content creation, and task automation.

To address the pain points above, insurers can leverage a platform approach. Here’s how Salesforce’s intelligence capabilities can play a role, and how they integrate into industry-specific insurance solutions.

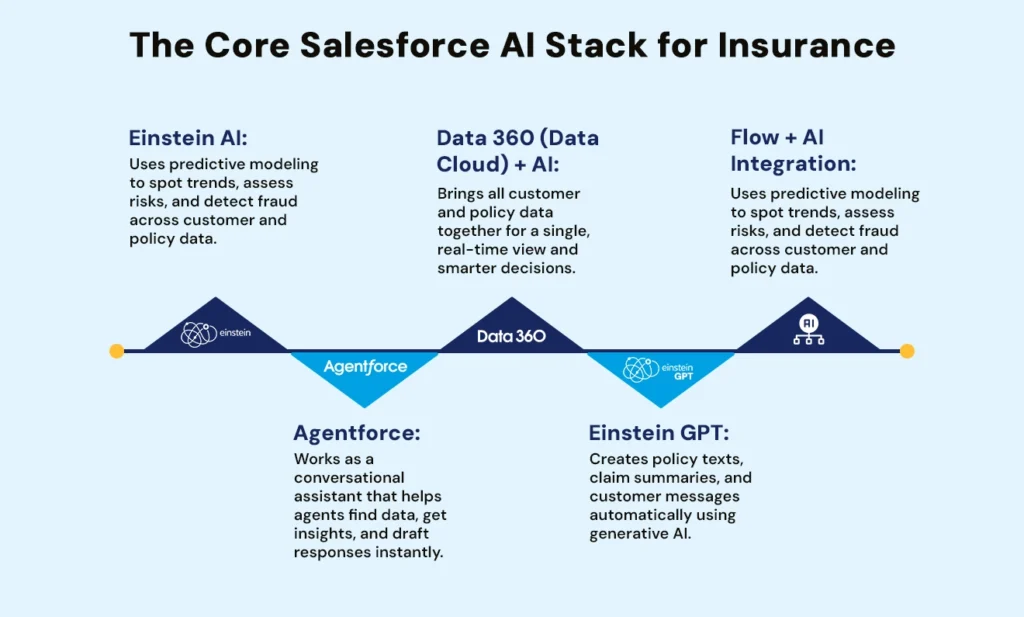

I. Einstein AI

Within the Salesforce ecosystem, the “Einstein” branding covers a range of AI capabilities. These include predictive modeling, natural language processing (NLP), and machine learning embedded in the application layer. For insurers, that means you can use Einstein in Sales Cloud, Service Cloud, and Marketing Cloud to spot patterns in customer behavior, predict churn risk, surface next-best-actions, and detect anomalies in claims data. This is part of how Salesforce’s artificial intelligence becomes operational rather than hypothetical.

Fun Fact: Salesforce Einstein delivers over 80 billion AI-powered predictions every day!

II. Agentforce

Agents and underwriters often need data in real time, contextually, and without switching systems. Agentforce serves as a conversational AI assistant embedded in Salesforce workflows. It can help surface key data points during a conversation, suggest policy options, draft communications, or propose underwriting guidance. This makes the agent’s experience smoother and helps enterprises scale their advisory model.

III. Data 360 + AI

One of the big obstacles in insurance is the fragmented data we discussed. Salesforce’s Data 360, formerly known as Data Cloud, offers a unified view of customer, policy, claims, and behavioral data in real time. With that unified layer, AI models (via Einstein or other frameworks) can operate on a richer, fresher dataset. In doing so, Salesforce AI implementation is not shoe-horning automation into a legacy infrastructure but using a reengineered data foundation.

IV. Einstein GPT

Generative AI is rapidly moving from novelty to utility. Within Salesforce, Einstein GPT enables underwriting teams to generate personalized policy documents, communications, claims summaries, or marketing outreach at scale. For example, an insurer might automatically generate an explanation of benefits tailored to the policyholder’s recent claim, with plain-language wording and relevant next steps. This marks a new frontier in Salesforce generative AI consulting: not just analytics, but creation.

V. Flow + AI integration

Automation platforms such as Salesforce Flow allow insurers to orchestrate processes, including when a claim is submitted, trigger document extraction, feed it into a risk model, route it to the appropriate adjuster, and generate a notification. When you combine Flow with AI capabilities (predictive scoring, NLP classification, anomaly detection), you get intelligent automation. This is where the idea of “automation with intelligence” becomes real.

VI. Financial Services Cloud and Insurance Data Model

Of course, applying generic CRM/AI engines isn’t enough. Salesforce offers industry-specific frameworks: the Insurance Data Model (IDM), which standardizes policy, claims, and underwriting data; and Financial Services Cloud for Insurance (FSCi), which provides pre-built objects, processes, and dashboards for insurers.

When you overlay AI capabilities onto that insurance-specific fabric, the value is amplified: the data structure matches the business, the rules are tailored, and the automation is relevant. Thus, Salesforce AI solutions in insurance become more than add-ons; they become embedded capabilities.

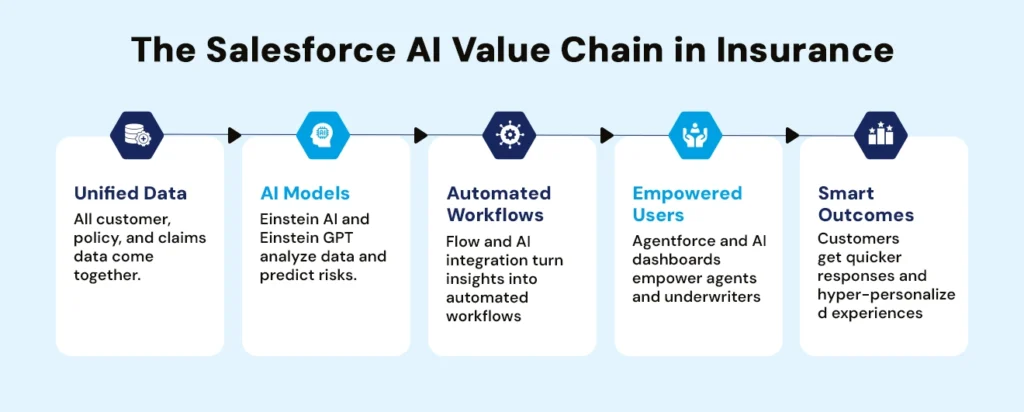

To summarize, Salesforce’s ecosystem enables insurers to move from fragmented data and manual processes to integrated intelligence, automation, and personalized engagement.

What Are the Real-World Use Cases of Salesforce AI in Insurance?

Let’s move from the conceptual information and see how AI in Salesforce really helps insurers. Salesforce AI has various use cases, ranging from underwriting automation to smart claims processing. Here are use cases where Salesforce’s AI capabilities shine for insurers.

a. Smarter Customer Engagement

“Salesforce is delivering a future where human and digital agents join forces to improve the customer experience,” – Kishan Chetan, Service Cloud General Manager at Salesforce.

With Einstein GPT generating tailored emails or messages, insurers can send renewal reminders or product offers that reflect each customer’s risk profile, behavior, and preferences.

Moreover, using Einstein predictive models, insurers can score a policyholder for renewal risk or identify upsell opportunities, so agents focus where value is highest.

When a service call comes in, the system pushes the most relevant recommendation to the agent in real time, whether it’s a cross-sell, a retention incentive, or a risk advisory.

These engagements raise relevance, speed, and customer satisfaction.

b. Intelligent Underwriting

About 81% of underwriting executives believe AI and generative AI will create new roles and make operations, risk assessment, and decision-making much more efficient. By analyzing historical claims, customer profiles, and external datasets (for example, telematics or climate data), insurers can develop risk models that vastly improve underwriting accuracy.

Using vision and NLP models (via Salesforce Flow + Einstein Vision/NLP), insurers can extract data from uploaded documents, identify discrepancies, and auto-populate underwriting systems. That means faster decisions and fewer manual mistakes.

c. Claims Processing Optimization

AI models analyze claims for anomalies, inconsistencies, and known fraud patterns, enabling early triage and special investigation. The impact: insurers can generate savings of 20% to 40% by integrating multimodal capabilities with AI and analytics.

AI also helps with smart triaging and routing. Upon receipt of a claim, a flow triggers document capture, damage image analysis(for property/auto), risk scoring, and routing to the correct adjuster.

Lastly, using Einstein GPT, insurers can generate a plain-language claim summary, draft communications to policyholders (“Your claim has been filed and we expect resolution by…”), and update portal notifications. This improves customer experience and reduces human workload.

d. Agent and Advisor Empowerment

Agentforce is a useful tool for agents, underwriters, and customer service reps. During a call or chat, an agent can ask “What’s this customer’s renewal history?” or “What upsell options apply given their last claim?” and get immediate, relevant suggestions. This boosts productivity and reduces training time.

If during any conversation, the customer mentions a change (such as a new vehicle or property), the system can recommend policy modifications, highlight risk gaps, and route it for approval, all within the same workflow.

e. Predictive Risk and Retention Management

With AI in Salesforce, insurers can identify customers likely to leave (based on behavior, interactions, and competitive offers) and proactively trigger retention offers.

For property/auto/health, combining IoT/telemetry data with AI yields dynamic risk scores. For instance, safe-driver telematics leads to a premium reduction.

Here’s a table summarizing the real-world applications of Salesforce AI:

Salesforce AI Use Cases Across Different Functions

| Function | Salesforce AI Tool | Business Impact |

|---|---|---|

|

Customer Engagement |

Einstein GPT |

Personalized renewal outreach |

|

Underwriting |

ML models |

Faster, more accurate risk scoring |

|

Claims Processing |

NLP and Vision |

Automated data extraction |

|

Agent Support |

Agentforce |

Real-time insights |

|

Policyholder Retention |

Predictive AI |

Early churn detection |

Taken together, these use cases illustrate how Salesforce AI solutions can deliver both operational improvement (faster, cheaper, fewer errors) and strategic value (better customer experience, personalized offers, new products).

How Can Insurers Adopt AI in Salesforce?

Adopting AI is not simply buying a license and switching it on. It requires planning, culture change, data strategy, governance, and alignment with business goals. For insurers looking at Salesforce AI implementation, here are a set of key steps:

Step 1: Define Your Business Objectives and Value Levers

Begin by asking critical questions such as what are the critical pain points we want to address? Is it faster claims processing, higher retention, better cross-sell, fraud reduction, and better underwriting accuracy? Define clear KPIs, for example, reduce claims turnaround by 30%, increase renewal rate by 8%, and reduce underwriting manual effort by 50%. Having concrete targets helps guide the rest of the program.

Step 2: Build a Unified Data Foundation

Fragmented data was earlier identified as a pain point. The CRM should unify customer, policy, claims, asset, and external risk data into a common data model (for example, by applying the Insurance Data Model inside Salesforce). Hence, choose an integrated CRM like Insura. Insura, as an AI-driven CRM built specifically for the insurance sector, goes beyond simple data storage. It centralizes policy, claim, customer, and agent data into a single view, creating an AI-ready foundation. This integrated platform instantly makes workflows smarter.

Insurers can further use Data 360 to bring real-time feeds. Without this foundation, AI models will be weak or siloed.

Step 3: Start with High-Impact, Manageable Use-Cases

Don’t attempt to automate everything at once. Pick a use-case with clear ROI and strong executive support. For example, you can begin with routing claims intake and document extraction, or predicting renewal risk. Implement the use-case end-to-end: data → model → workflow → outcome. Show quick wins to build momentum.

Step 4: Choose the Right Technology Stack and Partner

Since you are focusing on Salesforce, ensure your partner has experience in Salesforce AI consulting and implementation, as well as in the insurance domain. Ensure your licenses and architecture support the Einstein/AI components (Data 360, Service/Marketing/Underwriting Modules, and Flow). The partner should help map how AI integrates into existing workflows, rather than forcing a generic solution.

Step 5: Plan for Governance, Compliance, and Model Transparency

In insurance, risk and compliance matters. Ensure AI models are explainable, auditable, and compliant with regulatory standards. Automate compliance by establishing data governance (quality, lineage), model governance (validation, bias checking), and operational governance (who owns model performance, feedback loops). This is especially important if the automation touches pricing, underwriting, or claims of decisions.

Step 6: Prioritize Change Management and User Adoption

Tools alone don’t deliver value; users deliver value. Agents, underwriters, and adjusters must trust the system, feel its benefits, and adapt their workflows. Provide training, embedded AI-assisted assistants (like Agentforce) that complement users rather than replace them, communicate the “why,” and show early wins.

Step 7: Scale, Measure, and Iterate

Once initial use cases deliver results, plan for scaling. You may expand from claims to underwriting, from customer engagement to retention, from one line of business to others. Continuously monitor KPIs, gather feedback, refine models, and expand data sources (IoT, telematics, and third-party data). The objective is to shift from point solutions to a platform-level CRM powered by Salesforce Artificial Intelligence.

Step 8: Promote a Culture of Continuous Innovation

AI is not one-and-done. Risks evolve, customer behaviors change, and competition intensifies. Foster a culture in which data, models, insights, and automation are regularly reviewed, improved, and aligned with the business strategy. Encourage experimentation but govern experimentation. Reward outcomes as well as data maturity.

By following this roadmap, insurers can turn their CRM systems into strategic, intelligent platforms that deliver clear business outcomes rather than technology experiments.

What Is Next for AI-Driven Insurance?

Looking forward, the next era of insurance will be defined by three key shifts: predictive and proactive rather than reactive; dynamic instead of static; intelligent ecosystems rather than isolated systems. Platforms like Salesforce will play a central role in this.

The Road Ahead for AI-Augmented Insurance

| Area | Present | Future |

|---|---|---|

|

Claims Processing |

Automated workflows |

Fully self-learning resolutions |

|

Policy Pricing |

Fixed models |

Real-time dynamic pricing |

|

Risk Assessment |

Manual scoring |

AI and IoT-driven predictive modeling |

|

Customer Service |

Scripted chatbots |

Natural, context-aware Agentforce assistants |

Predictive, Proactive, and Personalized Insurance

Rather than waiting for a claim to occur, insurers will anticipate risk and intervene. With richer data (telemetry, embedded sensors, connected devices) and AI in Salesforce pipelines, insurers can trigger preventive actions. For example, a home insurer auto-detecting a frozen pipe risk and sending an alert; an auto insurer adjusting premiums mid-term based on safe driving. Customer experience becomes personalized, and the policyholder gets advice, not just a product.

IoT + AI + Salesforce Integration Powering Dynamic Pricing and Risk Prevention

The integration of IoT devices (sensors in vehicles, wearables in health insurance, and smart-home devices in property) with AI models and Salesforce platforms will enable dynamic, usage-based models. The insurer becomes a partner in risk management. Premiums adjust, offers evolve, and real-time signals drive decisions. This is not just “insurance as product,” but “insurance as service.”

Self-Learning Insurance Ecosystems That Continuously Adapt

In the future, models will restrain themselves, workflows will adapt, and new data sources will be automatically plugged in. A policyholder’s behavior, risk environment, and external events (climate, cyber) feed back into the system. The insurance CRM become a living ecosystem. At that point, Salesforce AI solutions are no longer add-ons; they become the insurer’s core architecture.

Responsible, Trusted AI for the Insurance Sector

With these advances comes responsibility. Insurers must proceed with care: model bias, transparency, regulatory scrutiny, and data ethics all matter. For example, the Financial Conduct Authority (FCA) in the UK has warned that AI-enabled hyper-personalization could render some customers “uninsurable”.

At the same time, trust in AI models is a prerequisite for customer acceptance. Without governance and auditability, the promise falls flat. As insurers adopt AI at scale, they must embed controls, oversight, and ethical guardrails.

The Evolving Role of the Insurer

Finally, the insurer’s role is shifting from simply paying claims to managing risk, from reacting to guiding, from product selling to service partnering. The use of Salesforce AI implementation helps enable that shift. Insurers who cling to the legacy model may struggle; those who embrace the intelligent platform will lead.

Did You Know? The global AI in insurance market is expected to reach $4.8 billion by 2032, growing at an 80% CAGR.

Conclusion

The insurance industry is at a high point. The convergence of data, automation, customer expectations, and risk complexity demands a new architecture. In this age, the question isn’t if insurers adopt AI, but how they adopt it: with purpose, strategy, and scale.

Platforms like Salesforce, when paired with its AI capabilities, provide the foundation for transformation, from unified data to predictive models to automated workflows, to empowered users and personalized experiences.

In doing so, insurers position themselves not just as carriers but as advisors, partners, and risk managers. They earn customers’ trust, reduce costs, improve outcomes, and stay competitive in a rapidly shifting world.

In short, embrace AI in Salesforce not as a gimmick, but as the backbone of your next-generation insurance enterprise. With the right roadmap, Salesforce AI solutions can deliver far more than automation; they can drive growth, differentiation, and long-term value.